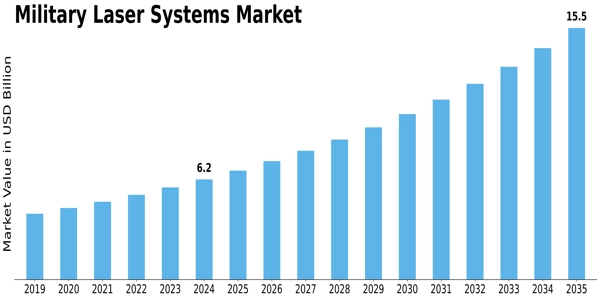

The Military Laser Systems Market is highly diversified, spanning multiple technologies, product types, and applications, each contributing to the broader expansion of the global defense laser ecosystem. According to (MRFR), the market was valued at USD 6.194 billion in 2024 and is projected to reach USD 15.46 billion by 2035 at a CAGR of 8.67%.

One key dimension of market segmentation is product type. The MRFR report highlights that the market encompasses a range of products such as laser designators, LIDAR systems, 3D scanners, laser weapons, laser range finders, ring laser gyros, and laser altimeters. Each of these contributes unique capabilities to military operations. Laser designators, for instance, provide precision targeting support, while laser weapons and range finders enhance defensive and offensive effectiveness with high-speed precision engagement.

From a technology perspective, multiple laser forms are shaping market growth. These include fiber lasers, solid-state lasers, chemical lasers, CO2 lasers, semiconductor lasers, and other emerging laser technologies. Among these, solid-state lasers are rapidly gaining traction due to their higher reliability, lower energy requirements, and adaptability to varied mission profiles — from target tracking to defensive countermeasures.

Application segmentation is another critical factor. The market includes applications such as target designation and ranging, guiding munitions, directed energy weapons, defensive countermeasures, and others. Defensive countermeasures currently dominate because these applications deliver crucial capabilities for threat neutralization and air defense. Laser systems in this segment can engage distant or fast-moving threats with precision and minimal collateral damage, aligning with modern military priorities.

Geographically, North America holds the largest share of the Military Laser Systems Market, accounting for approximately 45% of the global market share. This dominance stems from extensive military budgets, robust R&D investment, and the presence of leading defense contractors that continuously innovate laser technologies. Strategic defense initiatives by governments further reinforce North America’s leadership in the sector.

Europe is also a major regional player, contributing around 30% of global market share. Growth in Europe is fueled by increasing geopolitical tensions, collaborative defense funding mechanisms, and strong aerospace and defense industries in countries like the United Kingdom, Germany, and France. Collaborative programs and joint ventures are enhancing technological capabilities across the region.

The Asia-Pacific region is emerging as one of the fastest-growing markets due to heightened military modernization efforts, increasing defense budgets, and the strategic acquisition of advanced laser systems by China, India, Japan, and other regional powers. These developments reflect broader regional security dynamics and defense priorities.

Finally, the Middle East & Africa (MEA) region, while currently smaller, is gradually increasing investments in laser technologies to enhance defense readiness amid ongoing security concerns. Strategic defense procurements in countries like the UAE, Saudi Arabia, and South Africa are gradually boosting MEA’s market presence.

Overall, this segmented view underscores how diverse product types, technologies, applications, and regional dynamics are collectively shaping the Military Laser Systems Market’s strong growth trajectory.

Related Report: