Diabetes Foot Ulcers Treatment Market: Growth, Innovation, and Strategic Outlook (2025–2032)

Market Introduction

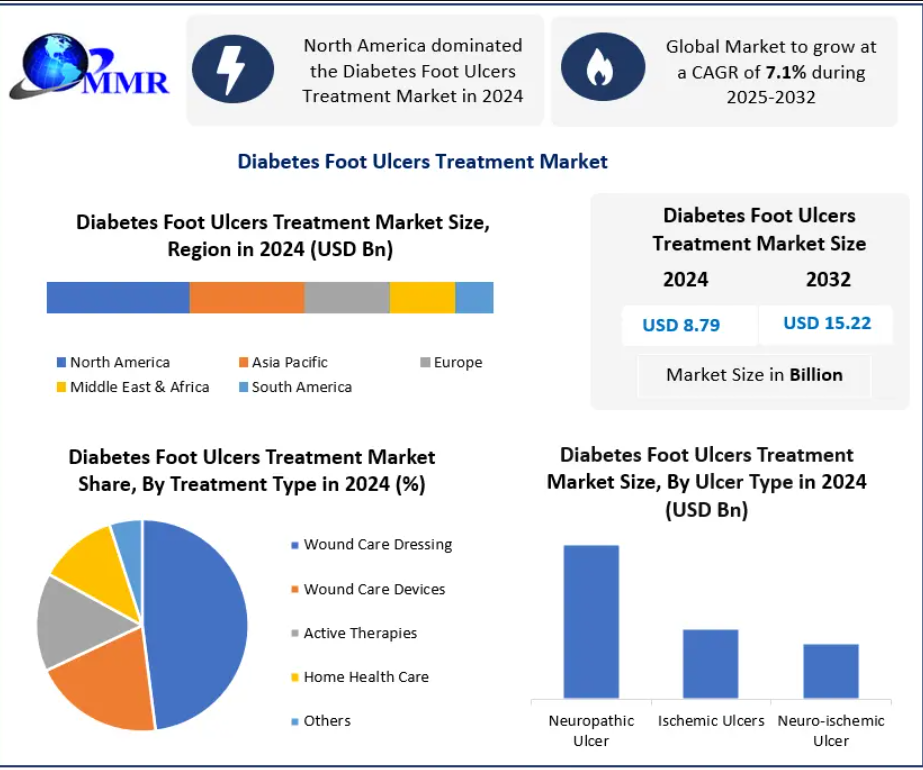

The global Diabetes Foot Ulcers (DFU) Treatment Market represents a critical segment within chronic wound management and diabetes care. In 2024, the market was valued at USD 8.79 billion , and it is projected to expand at a CAGR of 7.1% from 2025 to 2032 , reaching approximately USD 15.22 billion by 2032 . This growth trajectory reflects the mounting clinical and economic burden of diabetes, combined with rapid technological innovation in wound care therapies and medical devices.

Diabetic foot ulcers remain one of the most serious complications of diabetes, affecting nearly one in four diabetic patients during their lifetime. These ulcers significantly increase the risk of infection, hospitalization, and lower-limb amputation, making effective and timely treatment essential for patient outcomes and healthcare system sustainability.

Get a sample of the report@ https://www.maximizemarketresearch.com/request-sample/98438/

Market Drivers and Growth Catalysts

Rising Global Diabetes Prevalence

The primary driver of the DFU treatment market is the accelerating prevalence of diabetes worldwide. Lifestyle transitions, urbanization, aging populations, and increasing obesity rates continue to expand the diabetic patient base, directly enlarging the pool of patients at risk for foot ulcers. Emerging economies in Asia Pacific, Latin America, and the Middle East are witnessing particularly rapid growth in diabetic populations, strengthening long-term demand for DFU therapies.

Technological Progress in Wound Care

Advances in wound care science are reshaping treatment standards. Innovations in advanced dressings, negative pressure wound therapy (NPWT), bioengineered skin substitutes, growth factors, and regenerative therapies are improving healing rates while reducing complications and amputation risks. Emerging techniques such as 3D bioprinting, electrospinning scaffolds, and biosensing dressings are opening new frontiers in personalized wound management.

Shift Toward Early Detection and Proactive Care

Greater awareness among clinicians and patients regarding early diagnosis, infection control, and multidisciplinary care has enhanced treatment penetration. Preventive foot care programs, diabetic foot clinics, and patient education initiatives are reducing severe ulcer progression, while expanding demand for monitoring devices and home-based care solutions.

Integration of Digital Health and Telemedicine

Remote monitoring, teleconsultations, and connected wound care devices are transforming DFU management by enabling continuous assessment of wound status and timely clinical intervention. These digital platforms reduce hospital visits, lower readmission rates, and enhance adherence—making them an emerging growth segment within the market.

Competitive and Innovation Landscape

The competitive environment is characterized by continuous product launches, strategic collaborations, and technology-driven differentiation. Medical device manufacturers, biotechnology firms, and wound care specialists are investing heavily in regenerative medicine, tissue engineering, and smart wound care platforms.

Quality improvement initiatives in hospitals, combined with strong regulatory encouragement for advanced therapies, are accelerating adoption. Partnerships between pharmaceutical companies, research institutions, and healthcare providers continue to generate novel treatment modalities that improve healing time and reduce complications.

Segment Analysis

By Treatment Type

Wound Care Dressings remain the dominant segment and are expected to maintain leadership through 2032. Modern polymeric and hydroactive dressings offer moisture control, antimicrobial protection, enhanced re-epithelialization, and patient comfort. Emerging biosensing dressings capable of monitoring exudate levels, bacterial load, and tissue regeneration are poised to redefine personalized wound care.

Wound Care Devices—including negative pressure therapy systems and ultrasonic debridement tools—represent a fast-growing segment driven by hospital adoption and outpatient procedures.

Active Therapies, such as growth factors and bioengineered skin substitutes, are gaining momentum due to superior healing outcomes in chronic and non-healing ulcers.

Home Healthcare is expanding rapidly as healthcare systems promote outpatient management, cost containment, and patient-centric care models.

By End User

Hospitals dominate the end-user landscape, supported by multidisciplinary diabetes teams, specialized inpatient care units, and advanced diagnostic and monitoring infrastructure. The integration of electronic patient records, inpatient dashboards, and video consultation platforms has strengthened hospitals’ central role in DFU management.

Clinics, ambulatory surgical centers, and homecare settings are steadily increasing their share as minimally invasive procedures and decentralized care models gain acceptance.

Get a sample of the report@https://www.maximizemarketresearch.com/request-sample/98438/

Regional Outlook

North America

North America leads the global market, driven by a high prevalence of diabetes, well-established healthcare infrastructure, and strong reimbursement frameworks. The United States remains the epicenter of innovation, supported by substantial R&D investment and early adoption of advanced wound technologies.

Europe

Europe holds a significant share, anchored by mature healthcare systems in Germany, France, and the United Kingdom. Strong collaboration between research institutions and medical device companies, along with regulatory support for advanced therapies, underpins steady regional growth.

Asia Pacific

Asia Pacific represents the fastest-growing region. Countries such as India, China, Indonesia, and Japan are witnessing rapid increases in diabetic populations and healthcare spending. Expanding hospital networks, government awareness campaigns, and improving access to advanced wound care technologies are positioning the region as a major future growth engine.

Middle East & Africa and South America

The Middle East & Africa region is emerging as a promising market, supported by healthcare infrastructure development and rising diabetes awareness. In South America, Brazil and Argentina lead regional demand, driven by urbanization and growing adoption of modern wound care practices.

Key Industry Participants

The market is led by a mix of global medical technology leaders and specialized wound care companies, including:

- Medtronic plc

- Becton, Dickinson and Company (BD)

- Cardinal Health, Inc.

- Integra LifeSciences Corporation

- Ethicon (Johnson & Johnson)

- Organogenesis, Inc.

- Smith & Nephew plc

- 3M Healthcare

- Mölnlycke Health Care AB

- ConvaTec Group Plc

- Coloplast A/S

- Terumo Corporation

These players focus on portfolio expansion, geographic penetration, and innovation-led differentiation to strengthen competitive positioning.

Future Outlook and Strategic Implications

The Diabetes Foot Ulcers Treatment Market is transitioning from conventional wound management towards precision, regenerative, and digitally enabled care models . Over the next decade, market expansion will be shaped by:

- Rising adoption of bioengineered tissues and smart dressings

- Integration of AI-driven wound assessment tools

- Expansion of outpatient and home-based care

- Increased public–private collaboration in chronic disease management

Companies that align innovation with affordability, clinical effectiveness, and digital integration will be best positioned to capture long-term value in this rapidly evolving market.

Conclusion

With a strong growth outlook, expanding patient base, and accelerating innovation, the global Diabetes Foot Ulcers Treatment Market stands at the forefront of chronic wound care transformation. Strategic investments in advanced therapies, personalized treatment approaches, and digital health integration will define the competitive landscape and drive sustainable growth through 2032.