The global Simulation Software Market is a high-growth sector, crucial for accelerating product development, optimizing complex processes, and reducing the dependence on expensive physical prototyping. Driven by the mandates of **Industry 4.0**, the rapid expansion of the **Electric Vehicle (EV)** and **Autonomous Driving** sectors, and the increasing adoption of **Digital Twin** technology, the market is transforming from a traditional engineering tool to a strategic business asset. Key market segments, such as **Electronic Simulation Software** and **Cloud Deployment**, are experiencing the most significant growth. North America maintains the largest market share due to its established R&D infrastructure, while the Asia-Pacific region is poised for the fastest expansion fueled by aggressive industrialization.

Market Overview

Simulation software enables the creation of virtual models to analyze, test, and predict the behavior of products or processes under various real-world conditions. It uses advanced computational methods, such as **Finite Element Analysis (FEA)** and **Computational Fluid Dynamics (CFD)**, to provide insights across structural, thermal, fluid, and electromagnetic domains. The adoption of simulation is fundamentally altering product development cycles by allowing engineers to iterate designs rapidly, identify potential failures early, and achieve optimal performance before committing to physical manufacturing. This shift is leading to substantial reductions in time-to-market and overall production costs.

Market Size & Forecast

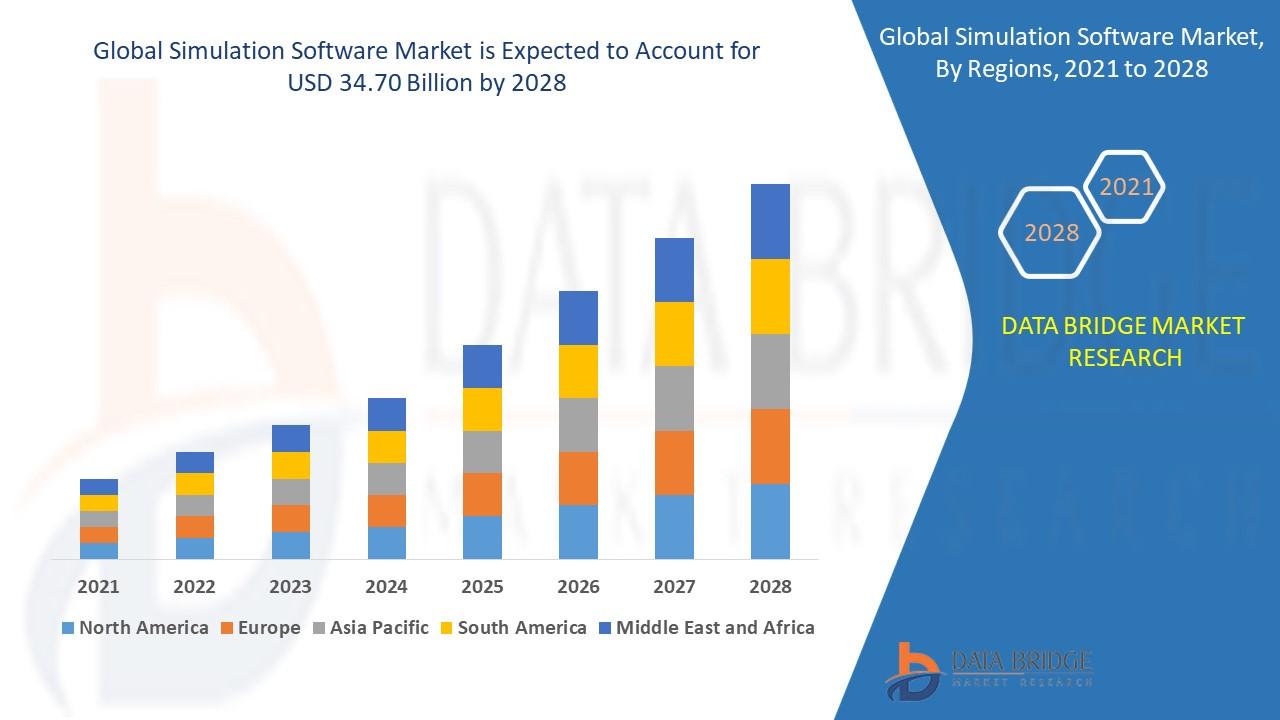

The global Simulation Software Market was valued at approximately USD 20.84 Billion in 2024 and is projected to reach an estimated value of USD 57.76 Billion by 2032. This robust expansion is anticipated to occur at a Compound Annual Growth Rate (CAGR) of 13.59% during the forecast period of 2025 to 2032. The primary factor driving this high CAGR is the increasing complexity of modern systems across all sectors, necessitating virtual validation and optimization.

Market Segmentation

The Simulation Software Market is segmented to provide detailed insights into product types, deployment models, and end-user verticals:

- By Component/Type:

- **Software** (Dominant Share): Includes FEA, CFD, Multiphysics, and Electronic Design Automation (EDA) Simulation.

- **Services**: Professional services (consulting, integration, training) and Managed Services.

- By Deployment Mode:

- **On-Premises**: Historically dominant, preferred by sectors with high-security needs for sensitive IP/data.

- **Cloud-Based** (Fastest Growing): Offers superior scalability, accessibility, and cost-efficiency, facilitating **High-Performance Computing (HPC)** for complex simulations.

- By End-User Vertical:

- **Automotive** (Largest Market Share): Driven by EV and autonomous vehicle R&D (crash testing, battery thermal management).

- **Aerospace & Defense**: Critical for complex systems modeling, flight simulation, and weapon system design.

- **Industrial Manufacturing**: Used for process optimization, robotics, and digital twin implementation.

- **Electrical, Electronics & Semiconductor**: Key for analyzing chip design, signal integrity, and electromagnetic interference.

- **Healthcare**: Used for medical device design, surgical planning, and pharmaceutical research (molecular simulation).

Regional Insights

Regional analysis highlights disparities in adoption maturity and growth rates:

- North America: Holds the largest market share (over 38%), characterized by high R&D spending, a strong presence of key technology vendors, and early adoption across the aerospace, automotive, and semiconductor industries.

- Asia-Pacific (APAC): Expected to be the fastest-growing region, with an estimated CAGR of 14.8%. This growth is spurred by rapid industrialization, increasing government investments in manufacturing (especially in China and India), and the swift adoption of smart factory initiatives (Industry 4.0).

- Europe: A mature market driven by stringent regulatory frameworks (e.g., environmental and safety norms) that necessitate simulation for compliance, particularly in the automotive and energy sectors.

Competitive Landscape

The Simulation Software Market is dominated by a few large, established vendors with comprehensive product portfolios, alongside niche players specializing in specific simulation types or verticals. Strategic **Mergers and Acquisitions (M&A)**, such as Synopsys' agreement to acquire Ansys, are shaping the competitive dynamics.

Key Market Players:

- Ansys, Inc.

- Dassault Systèmes SE (SIMULIA, CATIA)

- Siemens Digital Industries Software (Simcenter)

- The MathWorks, Inc. (MATLAB/Simulink)

- Altair Engineering, Inc.

- Autodesk, Inc.

- Synopsys, Inc.

- Hexagon AB

- PTC

Trends & Opportunities

- Digital Twin Technology: The shift toward creating persistent, real-time digital replicas of physical assets (Digital Twins) for predictive maintenance and operational optimization is the most significant growth opportunity.[Image of Digital Twin concept]

- AI and Machine Learning Integration: AI is being integrated to accelerate simulation setup, automate parameter optimization (**Generative Design**), and enhance the predictive accuracy of results, significantly reducing computation time.

- Cloud-Native Simulation (SaaS): The widespread adoption of Software-as-a-Service (SaaS) and hybrid cloud deployment models lowers the barrier to entry for Small and Medium Enterprises (SMEs) and facilitates seamless collaboration across global R&D teams.

- Multiphysics Simulation: Increasing complexity requires simultaneous modeling of multiple interacting physical phenomena (e.g., thermal-stress, fluid-structure interaction), driving demand for advanced multiphysics tools.

- Electrification and Autonomous Systems: The exponential growth in R&D for EVs, autonomous vehicles (AVs), and drones demands massive amounts of high-fidelity virtual testing and simulation for safety and performance validation.

Challenges & Barriers

- High Implementation and Licensing Costs: The significant upfront investment in licenses, specialized hardware (HPC clusters), and ongoing maintenance can be prohibitive, especially for smaller firms.

- Lack of Skilled Professionals: A persistent shortage of engineers and analysts with the specialized expertise required to effectively set up, run, and interpret complex simulation models acts as a restraining factor.

- Integration Issues: Difficulties in seamlessly integrating simulation tools with existing Product Lifecycle Management (PLM), Computer-Aided Design (CAD), and other enterprise systems can hinder full adoption.

- Data Security and IP Risk: Concerns over the security of highly sensitive intellectual property and proprietary design data, especially with the use of public or hybrid cloud deployment models.

Conclusion

The Simulation Software Market is indispensable to modern industrial and technological advancement. Its trajectory is firmly upward, fueled by the irreversible trends of digitalization, electrification, and autonomy across virtually all major industries. Future market leadership will be defined by companies that successfully integrate AI/ML into their solvers, expand their cloud-native offerings, and deliver robust, end-to-end solutions that seamlessly transition from product design (virtual prototyping) to operational phase (digital twin).

Browse Trending Report:

North America Torque Vectoring Market

North America Transcritical CO2 Market

Europe Transcritical CO2 Market

Asia-Pacific Transcritical CO2 Market

Middle East and Africa Transcritical Carbon Dioxide (CO2) Market

Middle East and Africa Unmanned Surface Vehicle (USV) Market

North America Unmanned Surface Vehicle (USV) Market

Europe UV Filter Market

Asia-Pacific UV Filter Market

Middle East and Africa UV Filter Market

North America UV Filter Market

Asia-Pacific Warm Water Aquaculture Feed Market

Europe Warm Water Aquaculture Feed Market

Middle East and Africa Warm Water Aquaculture Feed Market

North America Warm Water Aquaculture Feed Market

Contact Us

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email: [email protected]