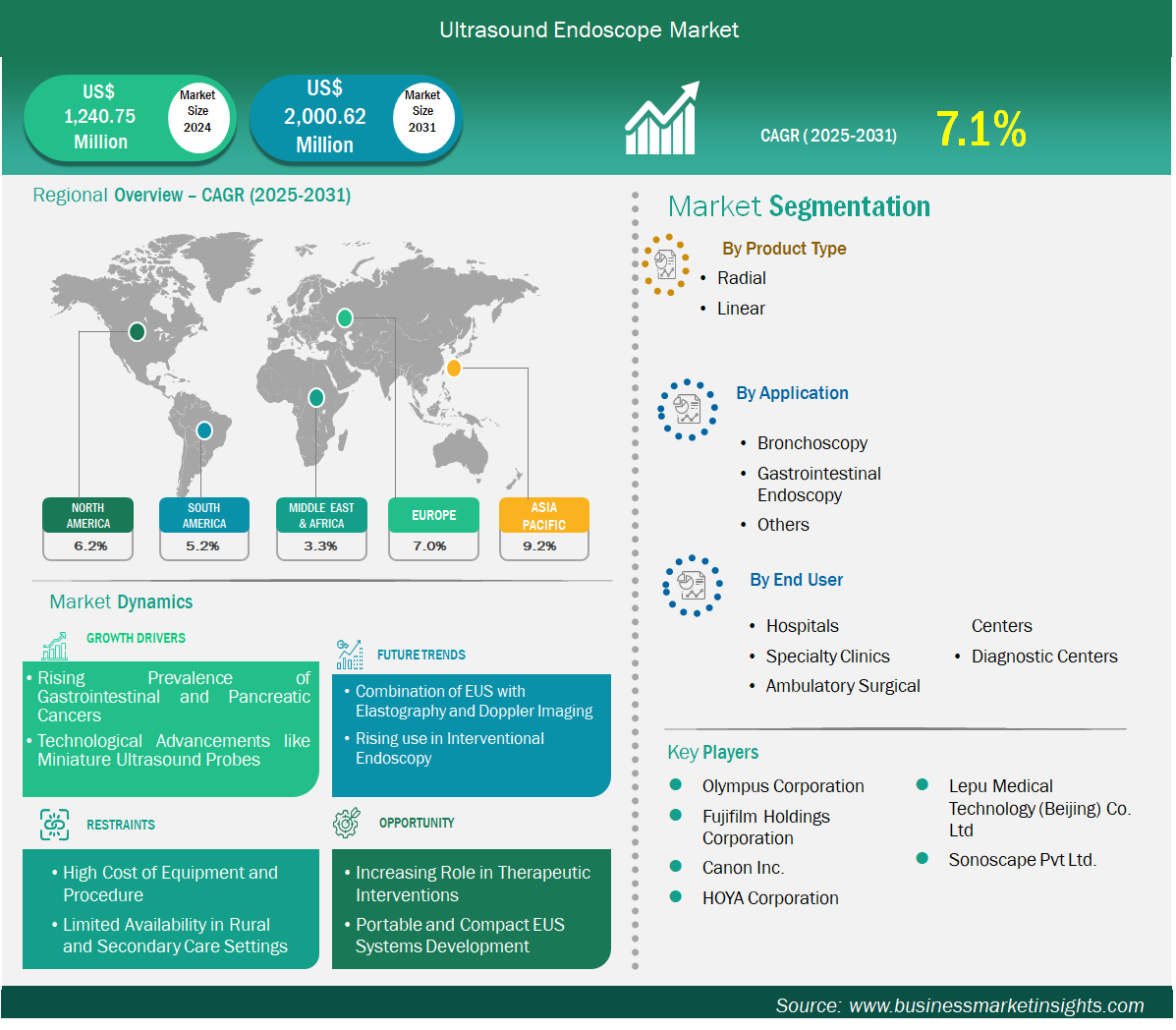

The global Ultrasound Endoscope Market is structured across three primary segmentation dimensions that together reveal the clinical, technological, and institutional drivers of market performance. This Ultrasound Endoscope Market Report examines product type, application, and end user segments across a market growing from US$ 1,240.75 million in 2024 to US$ 2,000.62 million by 2031 at a CAGR of 7.1%.

Request Sample Pages of this Research Study @ https://www.businessmarketinsights.com/sample/BMIPUB00031683

By Product Type, the market is divided into Radial and Linear segments. The Linear segment dominated in 2024. Linear ultrasound endoscopes are preferred because they enable real-time imaging alongside fine-needle aspiration in a single procedural session, offering both diagnostic and interventional capabilities across gastrointestinal and pulmonary applications. Their ability to guide therapeutic interventions without requiring a separate procedure is a significant clinical and economic advantage that continues to drive their dominance. The radial segment, while secondary in market share, remains clinically valuable for circumferential imaging that provides a comprehensive 360-degree view of surrounding structures, particularly in staging esophageal and rectal cancers.

By Application, the market covers Bronchoscopy, Gastrointestinal Endoscopy, and Others. Gastrointestinal Endoscopy led the market in 2024, driven by exceptionally high procedure volumes in pancreatic, esophageal, and gastric diagnostics where EUS provides unmatched imaging depth and biopsy access. Bronchoscopy is a strong secondary application, with endobronchial ultrasound widely adopted for lung cancer staging and mediastinal lymph node assessment. The Others category captures emerging and expanding applications across biliary, rectal, and urological endoscopy that are progressively broadening the clinical footprint of ultrasound endoscopes.

By End User, the market includes Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Diagnostic Centers. Hospitals led in 2024, benefiting from advanced infrastructure, specialist gastroenterology and pulmonology teams, and high patient volumes requiring complex diagnostic and minimally invasive procedures. Specialty clinics are growing as a segment as EUS technology becomes more compact and accessible. Diagnostic centers represent an important emerging end user category, particularly in Asia-Pacific where standalone diagnostic facilities are expanding rapidly in response to rising cancer screening demand. Ambulatory surgical centers are expected to gain share through the forecast period as outpatient-optimized EUS platforms become commercially available.

About Us

Business Market Insights is a one-stop industry research provider of actionable intelligence. Specializing in industries including Manufacturing and Construction, Semiconductor and Electronics, Healthcare, and more, the firm publishes over 500 research reports annually.

Contact Us

If you have any queries about this report or if you would like further information, please contact us: Phone: +16467917070 E-mail: [email protected]